Term Life Insurance

Term life insurance offers simple, affordable protection designed to cover your loved ones during the years they need it most. With low monthly premiums and flexible coverage lengths—typically 10, 20, or 30 years—term insurance provides high death-benefit protection without complicated features or added costs.

Key Features and Benefits of Term Life Insurance

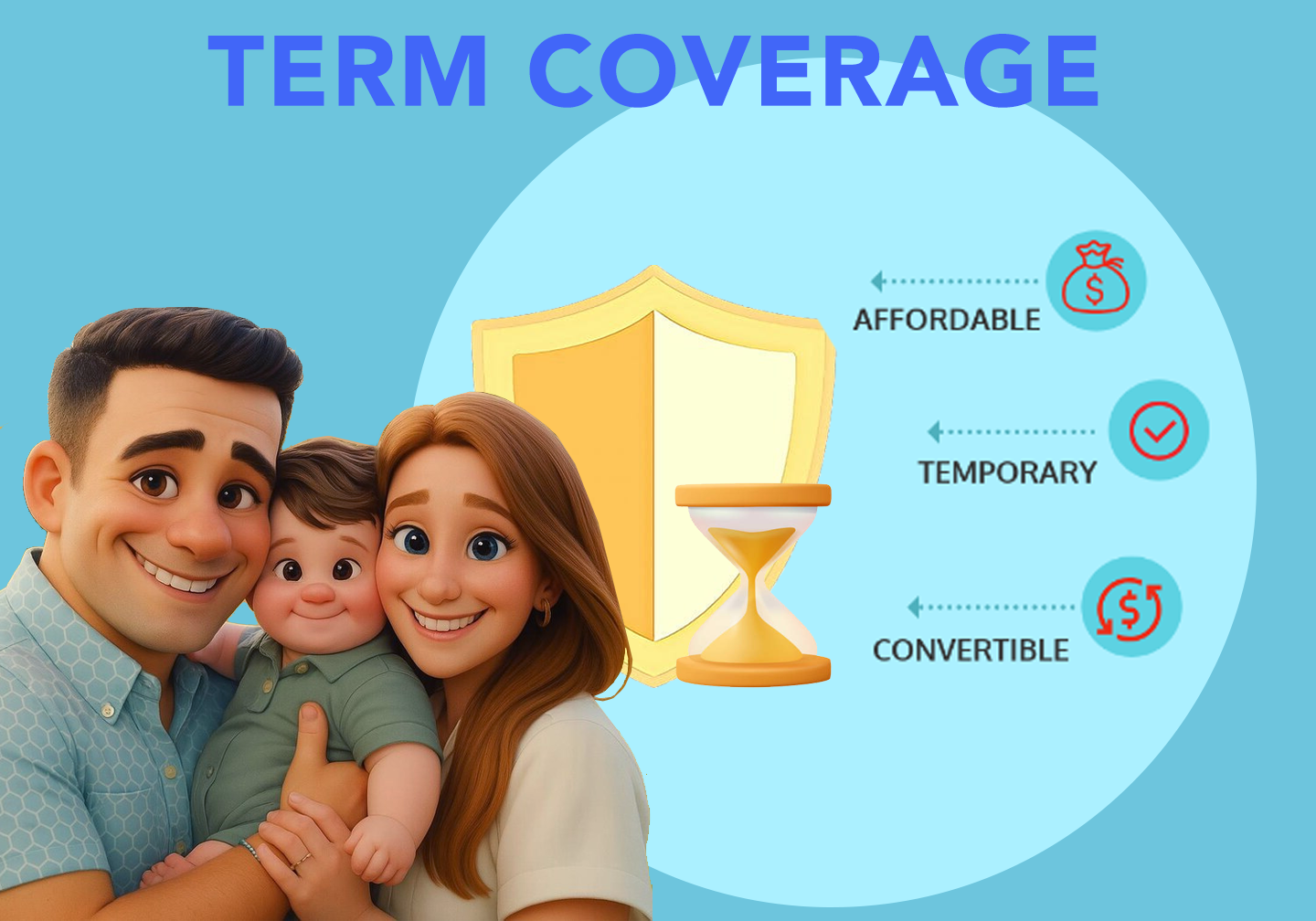

Term life insurance offers reliable, affordable protection designed to cover you during the years when financial responsibilities are highest. It is ideal for people who need strong, time-limited security without the higher premiums of permanent insurance. With minimum rate protection, term policies provide some of the lowest premiums in the industry while still delivering high coverage amounts, making them a cost-effective way to protect your family. One of its greatest advantages is liability protection—term insurance can cover major obligations such as mortgages, car loans, credit lines, or business debts so these responsibilities don’t fall on loved ones. It can also be used for SBA and other loan requirements, providing lenders with reassurance that the balance will be paid in the event of an unexpected death.

Many individuals choose term insurance during their early earning years or business-building stages because it offers meaningful coverage while keeping costs low. It supports mortgage protection, ensuring your home remains secure for your family, and it can provide funding for final expenses, helping cover funeral costs or outstanding bills without financial strain. Whether you need temporary coverage while raising a family, building a business, securing a loan, or protecting long-term assets, term life insurance delivers flexible, straightforward, and budget-friendly security for the exact period you need it most.

PROS & CONS OF TERM LIFE INSURANCE

PROS

CONS

What is Term Life Insurance ?

Term life insurance is a simple, affordable type of life insurance designed to provide financial protection for a specific period—typically 10, 20, or 30 years. During this term, if the insured person passes away, the policy pays a tax-free death benefit to their beneficiaries, helping cover living expenses, debts, mortgages, education costs, or other financial needs. Term insurance is popular because it offers high coverage at low monthly premiums, making it a practical choice for families, homeowners, and business owners who want strong protection without the higher cost of permanent life insurance. With clear, straightforward features and no cash value component, term life insurance delivers dependable security exactly when it’s needed most.

Key Takeaways

Affordable Protection: Term life insurance offers high coverage at low monthly premiums.

Simple & Clear: Pure protection with no cash value or investment components.

Time-Based Coverage: Designed to protect you for a set period—10, 20, 30 years, or more.

Income & Debt Protection: Helps cover mortgages, loans, living expenses, and family needs if you pass away.

Tax-Free Benefit: Pays a tax-free death benefit directly to your beneficiaries.

Flexible Options: Easy to match with major milestones like raising a family, buying a home, or starting a business.

Convertible: Many policies allow you to convert to permanent coverage later, without a medical exam.

“

Get personalized, free, no-obligation term life quotes. Enter your information, check eligibility, and speak with an agent if you need guidance. It costs $0 to find coverage that fits your budget. Compare prices and options in minutes and receive term life insurance estimates in as little as 5 minutes.

How Does Term Life Insurance Work?

Term life insurance provides affordable financial protection for a set period—typically 10, 20, or 30 years—offering your family a guaranteed death benefit if you pass away during the term. It’s one of the simplest forms of life insurance, with no cash value component, making premiums lower and easier to budget. You choose the coverage amount and length, and as long as premiums are paid on time, your beneficiaries receive a tax-free payout that can cover mortgage payments, debts, income replacement, or future expenses. Because of its flexibility, low cost, and straightforward structure, term life insurance is a smart option for families looking for reliable coverage without long-term commitments.

Key Features

Fixed Coverage Period – Term life insurance provides protection for a set number of years, such as 10, 20, or 30, ensuring your family is covered during critical financial periods.

Affordable Premiums – Without a cash value component, term policies are generally much more budget-friendly compared to whole or universal life insurance.

Guaranteed Death Benefit – If you pass away during the policy term, your beneficiaries receive a tax-free payout to cover debts, living expenses, or future financial goals.

Flexible Term Options – Choose a policy length that aligns with your financial responsibilities, like paying off a mortgage, funding education, or income replacement.

Renewable and Convertible – Many term policies can be renewed after the term ends or converted to permanent life insurance without a medical exam.

Simple and Transparent – Term life insurance is straightforward, easy to understand, and ideal for those seeking coverage without complicated investment or cash value features.

Who Needs a Term Life Insurance Policy?

It’s impossible to list every position in which someone should get term life insurance. However, we highlighted the cases when people usually get it.

- Business owners use it to pay off debts, outstanding taxes, and expenses for their business.

- People with outstanding loans can use term life insurance to pay off their debt.

- Stay-at-home parents can use their policy as an income replacement or pay expenses such as childcare.

- Young and newlywed couples can benefit from term life coverage because their rates will be lower. Proceeds can be used for anything from replacing income to repaying off student loans and covering future expenses like education costs for their children.

Advantages

- Straightforward and uncomplicated. It’s easy to apply, and most commonly, people don’t need help from professionals because it’s obvious to manage.

- Less expensive. Monthly expenses are lower than with permanent life insurance. Remember that you don’t get the same product, so it’s not strange that they don’t cost the same.

- Tax-free death benefit. If the policyholder dies while the policy is active, their beneficiaries will receive money that will not be taxable.

- Multiple policy options and flexible payment. Applicants can choose how long they need coverage, from one to 30 years. They also can decide when they’ll pay premiums – monthly, quarterly, semi-annually, or annually.

- No penalty for canceling. If an individual cancels a term policy while it’s active, there wouldn’t be any fees or penalties.

Disadvantages

Upper age limit. This limit depends from company to company. But people up to age 50 are usually allowed to apply for all term lengths. People who are 60 or older can only use ten or 20-year-term.

Temporary coverage. We will cover later in the article benefits of permanent coverage, but most people prefer it over temporary coverage. There is a danger that an individual could suffer health reverses and be uninsurable when the term coverage expires.

No cash value. With term life insurance, you can’t build cash value; if you cancel it, you won’t get any money back.